Oil Context Weekly (W4)

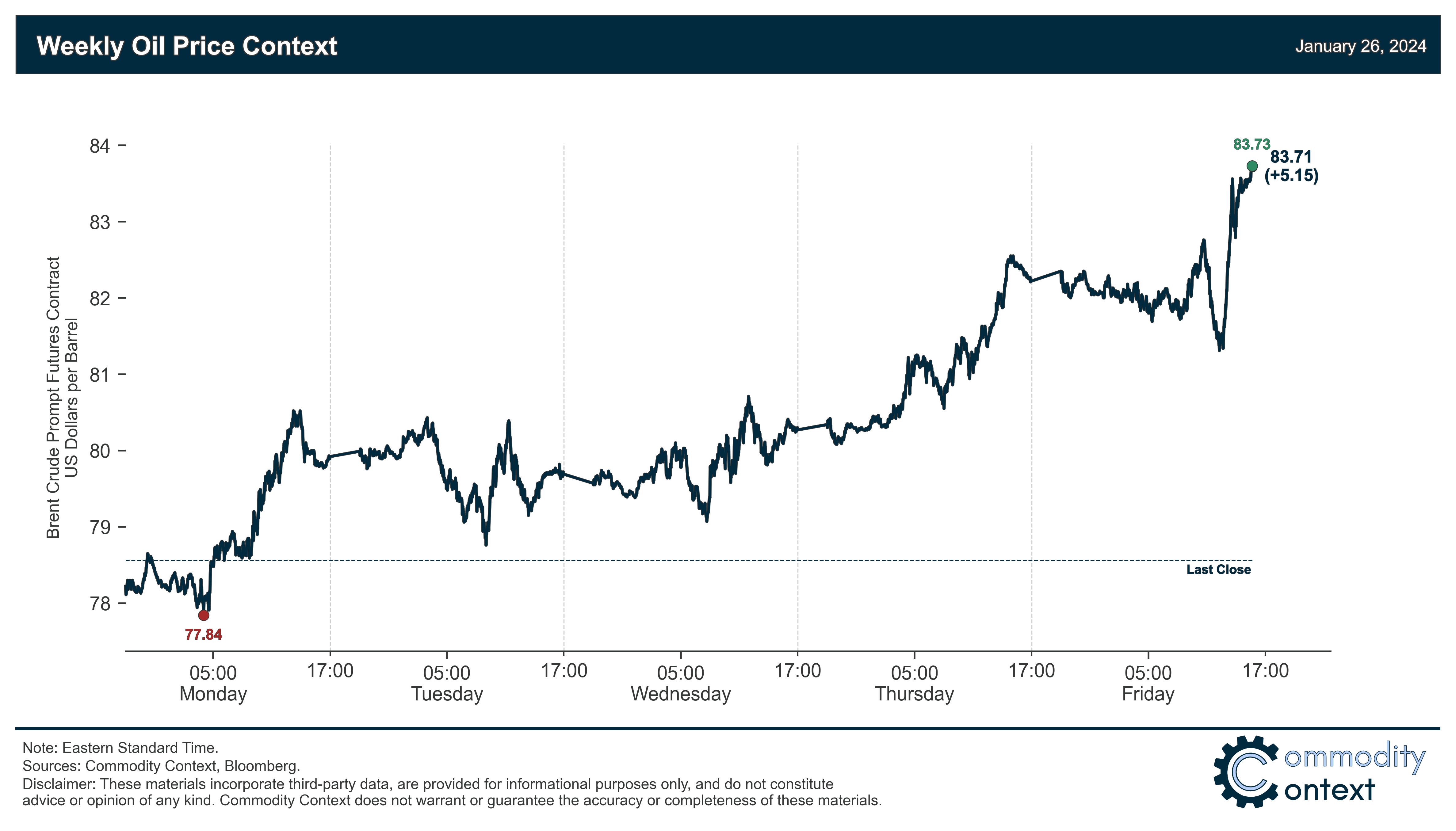

Crude prices roared $5/bbl higher as spot markets tightened on logistical disruptions, receiving a final Friday boost following confirmation of a major Houthi attack on a British naphtha tanker.

Heads up to Albertan Commodity Context subscribers, I’ll be in Calgary during the week of February 19th—I’d love to meet up with subscribers looking to discuss the latest oil market developments over drinks, so please let me know if you’re interested here (Google Form) so I can get a sense of numbers.

Had the opportunity to join BNN Bloomberg for a conversation about this latest global crude market rally as well as the outlook for Western Canadian Select crude prices following the startup of the much-delayed Trans Mountain Expansion pipeline—check out that full interview here.

Happy Friday, Commodity Context Subscribers!

Every week, I summarize developments in flat crude prices, calendar spreads, high-frequency inventories, refined products, and positioning data, as well as a taste of the themes I’ve been thinking about or following closely.

If you’re already subscribed and/or appreciate the free chart and summary, hitting the LIKE button is one of the best ways to support my ongoing research.

Summary

Flat Prices roared $5/bbl higher to just shy of $84/bbl (Brent) for the best weekly gain since the October rally that followed the onset of the Israel-Hamas war as steadily-tightening spot markets got a final Friday shot in the arm in the form of a major Houthi attack on a British tanker.

Futures Curves tightened into deeper backwardation, although calendar spread gains slowed compared to last week’s notable gains and Brent CFDs traded sideways-to-down; so, the worst of the tightness stemming from Red Sea- and weather-related disruptions may be behind us—we’ll see if the latest Red Sea tanker news changes that calculus.

Inventories data was staggeringly bullish, revealing material stock draws across all major tracked hubs with all-time-high total petroleum draws in the US and crude declines in ARA Europe.

Refined Products markets are currently being driven by increased pressure in middle distillates markets emanating from Europe, which has seen its post-Russian-sanction supply—that largely transits north through the Suez Canal—disrupted by the ongoing Red Sea crisis and received a massive Friday boost following news of the tanker attack.

Investor Positioning data confirmed that speculators were net buyers of crude contracts over the past week-through-Tuesday, though gross short positions remain sizable and the covering of which will likely add upside pressure to crude rallies, much as we saw on Thursday and Friday.

As Well As more detail on this latest—and arguably most significant—Houthi tanker attack, the ongoing volumetric impact of North America’s cold snap, the restart of Libya’s largest oil field, attacks on Russia’s oil logistics infrastructure, and further clarity regarding the startup timeline of Canada’s Trans Mountain Expansion pipeline.