How Low Can Oil Inventories Go?

How Low Can Oil Inventories Go?

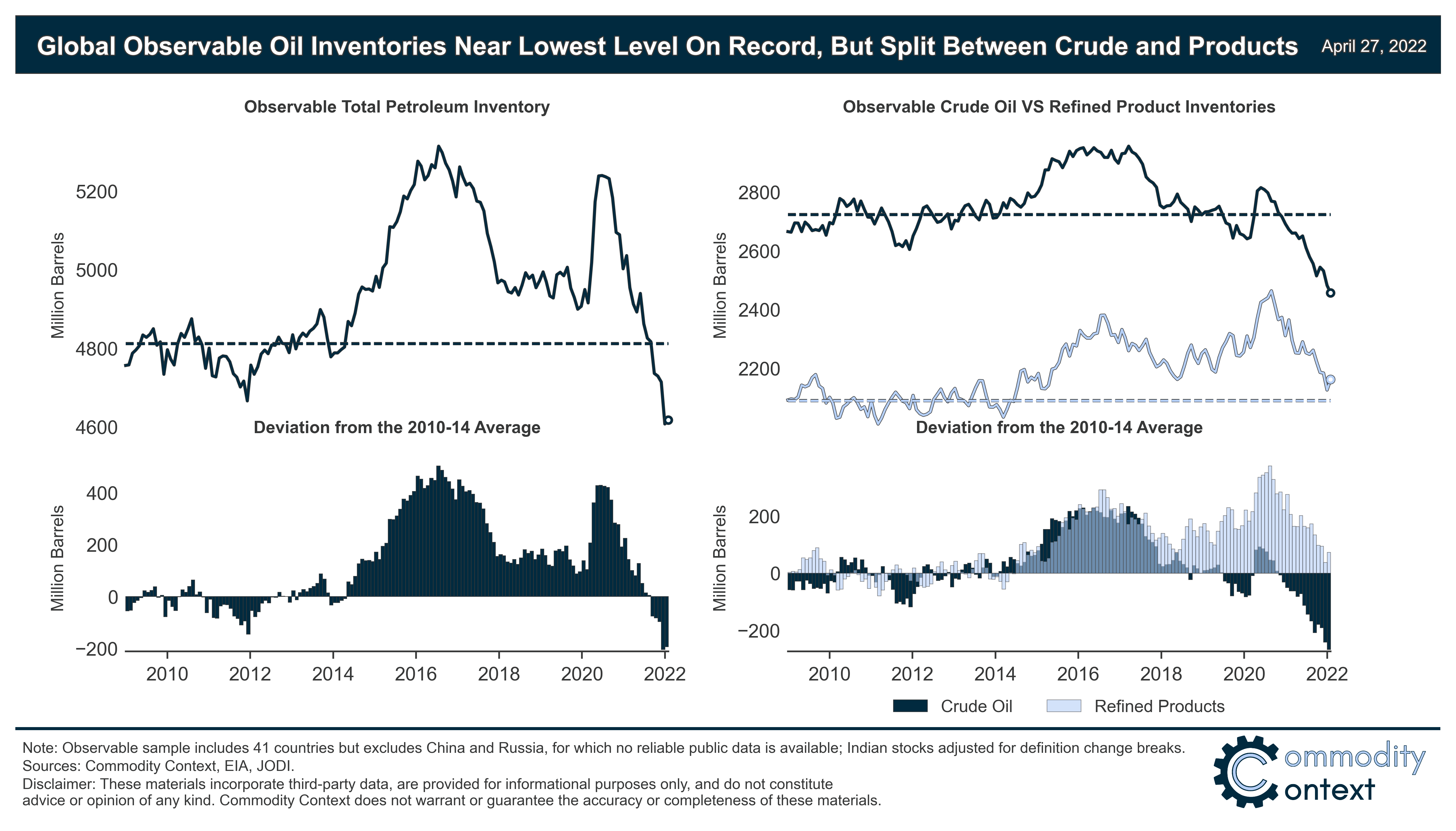

Observable global oil inventories have fallen at record pace, now lowest in more than a decade

Global observable oil inventories have fallen at their fastest pace on record over the past year and a half, plunging by more than 600 million barrels, as sluggish production growth failed to keep pace with rebounding demand.

Those inventories now sit at their lowest level in more than a decade and are definitively below the presumed “logistical requirement” or 2010-14 average, a period marked by chronically elevated oil prices.

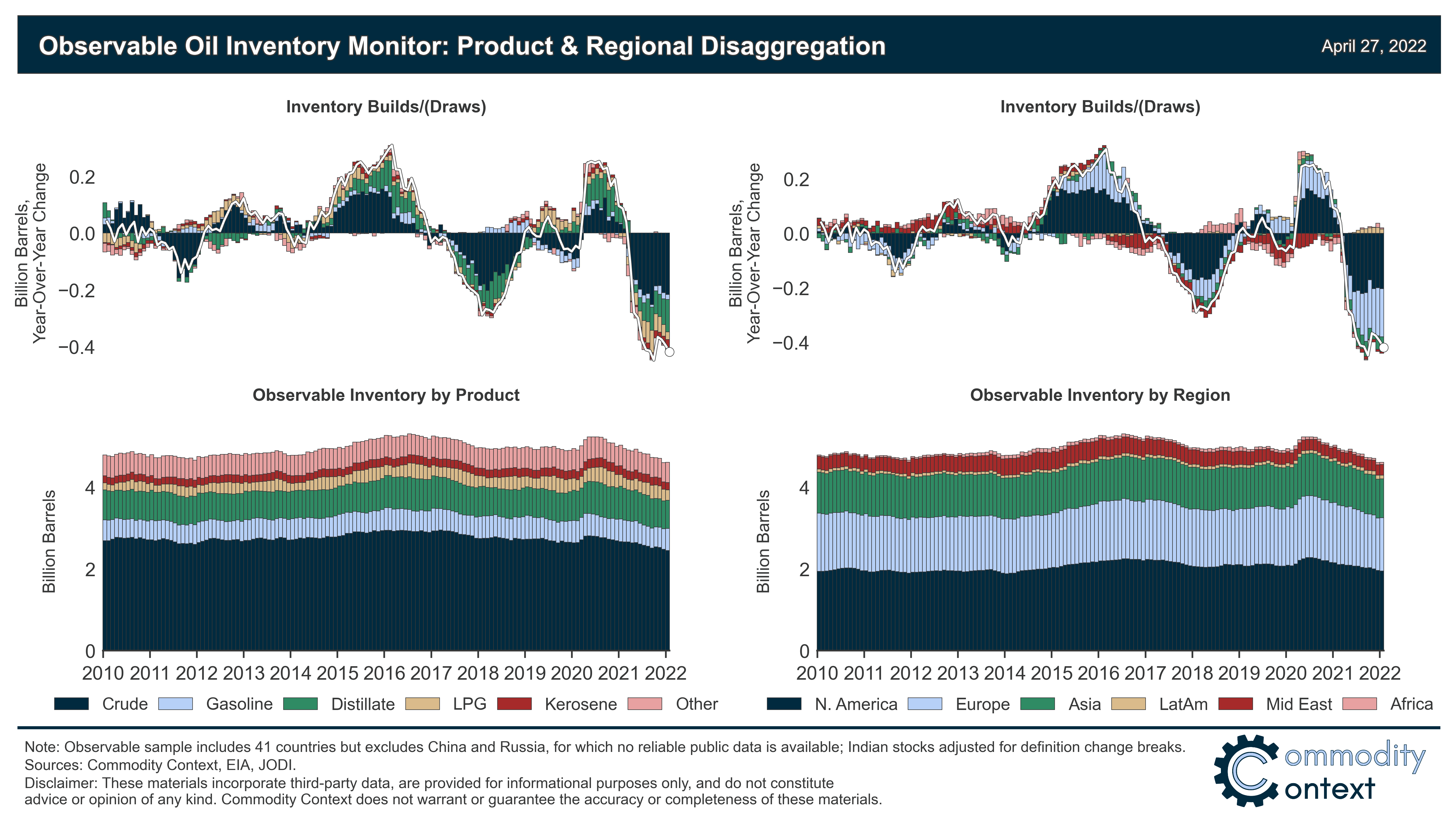

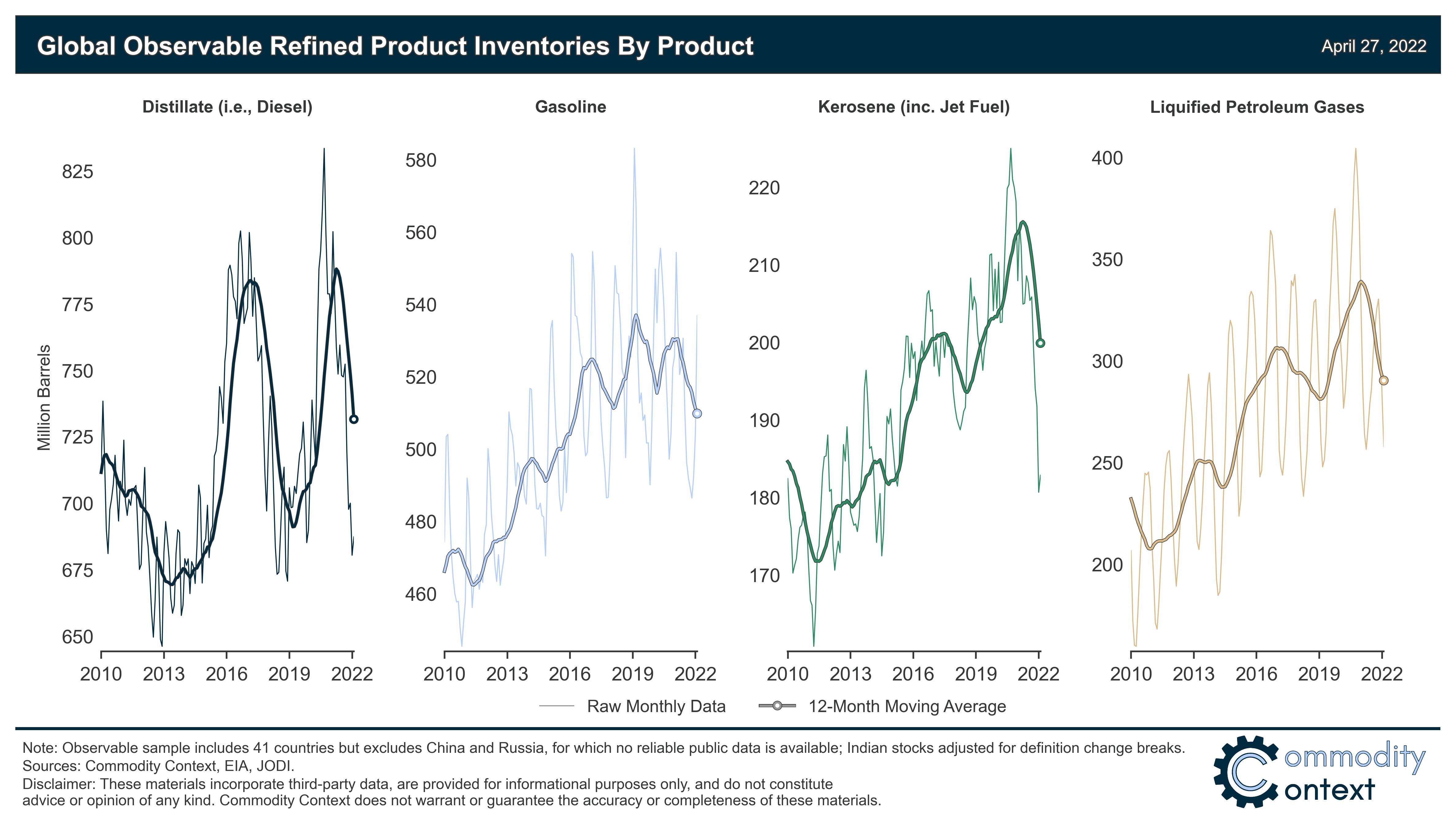

Crude inventories have fallen most drastically, while refined products remain slightly better stocked—however, within products middle distillates like diesel, gas oil, and jet fuel have experienced the steepest drawdown, which helps explain the wildly high refining margins witnessed for those fuels.

The oil market is the world’s largest physical stock and flow model. Every single day, roughly 100 million barrels of oil are produced and consumed globally. To ease the logistical chaos of supplying that volume in real time, oil market participants store large quantities of both crude oil and refined products to allow for a steadier stream of petroleum into refineries and out to consumers. Based on average observable inventory levels before the 2014-16 price crash, this logistical requirement seems to sit at around 4.8 billion barrels of crude and products as seen in the chart above.

This healthy store of inventory is held in the oil market’s steady-state to ensure more seamless operations and marketing—but inventories also serve a secondary purpose as overflow/shortfall insurance for times when the global supply and demand balance falls out of sync. The market has experienced two such convulsions in the past decade: the US shale-driven oversupply that glutted inventories and crushed oil prices between 2014-2016 and, of course, the COVID lockdown-induced demand collapse of early 2020.

Note: The “Global(ish)” sample assessed here covers commercial and government-held stocks in 41 inventory-holding countries but does not include China or Russia—both material holders of crude and product inventory—due to a lack of publicly available information. I have also adjusted Indian refined product data to account for data breaks related to definitional changes. More on these caveats below.

Oil’s Destock Can’t Stop, Won’t Stop

When COVID lockdowns demolished demand for transportation fuels, it prompted the fastest-ever inflow of inventories of both crude and products. Now we’re witnessing a drawdown in global petroleum inventories that is the steepest on record: stocks fell by more than 600 million barrels over the past year and a half at a sustained pace of more than one million barrels per day, and now sit around their lowest level in more than a decade.

To a somewhat lesser degree relative to crude, we’ve also seen large drawdowns in the inventory of refined petroleum products. Taken together, stocks of these finished fuels remain slightly above the 2010-14 average while crude is well below. That said, not all products are equally sanguine, with a substantial drawdown in middle distillate stocks including diesel, gas oil, and jet fuel, as seen in the chart below. This reality goes a long way in explaining the explosive refining margins commanded by these fuels at the moment over better-stocked products like gasoline.

But while inventories have drawn down a lot, it’s not necessarily a straightforward matter to assess if they’re yet reached critically low levels.

First, what is normal? In normal-ish markets, the typical measure is to compare inventories to their trailing 5-year average and high-low range given that we often see seasonality to these stocks. Unfortunately, this method has an obvious and fatal flaw: the longer you’re in an oversupplied market, the easier the 5-year average benchmark is to beat (e.g., the past years of oversupply make that 5-year average benchmark unreasonably high). To avoid this trap, in this piece I compare inventories to their 2010-14 level, a period that coincided with the high (>$100 per barrel) price environment most comparable to the rally that we’re witnessing today. On that basis, total petroleum inventories are about 200 million barrels below “normal”—roughly 270 million barrels below for crude, and about 70 million barrels above for refined products (see first chart at top of post).

Even so, there are challenges with using any historical averages at all. Most notably, the industry isn’t static: consumption has risen by more than 10 million barrels per day over the past decade. If you assume that the structural inventory requirement is a multiple of the system flow rate, it should also increase in line with rising demand. On the flip side, factors like the reduced shipping times due to US imports displaced by shale/Canadian production or the increased operational efficiencies of better inventory management could theoretically reduce the required flow multiple.

The Known Unknowns: China and Russia

There are a few more important caveats to this inventory story.

First, a note on observable inventory levels: one of the enduring challenges of fully assessing global inventories is that we can’t actually see them all—and, as per above, we have only spotty estimates for both Chinese and Russian petroleum inventory holdings.

Most notably, China is by-far the largest share of incremental global demand over the past decade and has built up a massive domestic inventory system—but this is outside the view of my observable inventory data. China does not and has not published publicly available inventory data. There are only estimates that Chinese oil inventories sit between 800 million and a billion barrels—though I am not able to independently verify these figures—with about a third of that comprising Beijing’s strategic stockpile of which much was accumulated during the past decade of glutted markets. Given this blind spot, we should, at the very least, avoid including Chinese demand when considering the sufficiency of visible stock and this is why I’ve opted to keep this inventory discussion in terms of nominal barrels rather than adjusted for “days of supply”.

Meanwhile, Russia no longer makes its oil inventory data public, but we know that more than a decade ago they were holding a few hundred million barrels of crude with a bit extra in products. This is a sizable sum that makes sense given the scale of Russia’s industry. We can anticipate that the invasion of Ukraine has likely pushed huge additional volumes into storage, as buyers dry up due to formal and informal sanctions, to the point that Russia will likely hit tank-tops this year and force production shut-ins (more on that in another post).

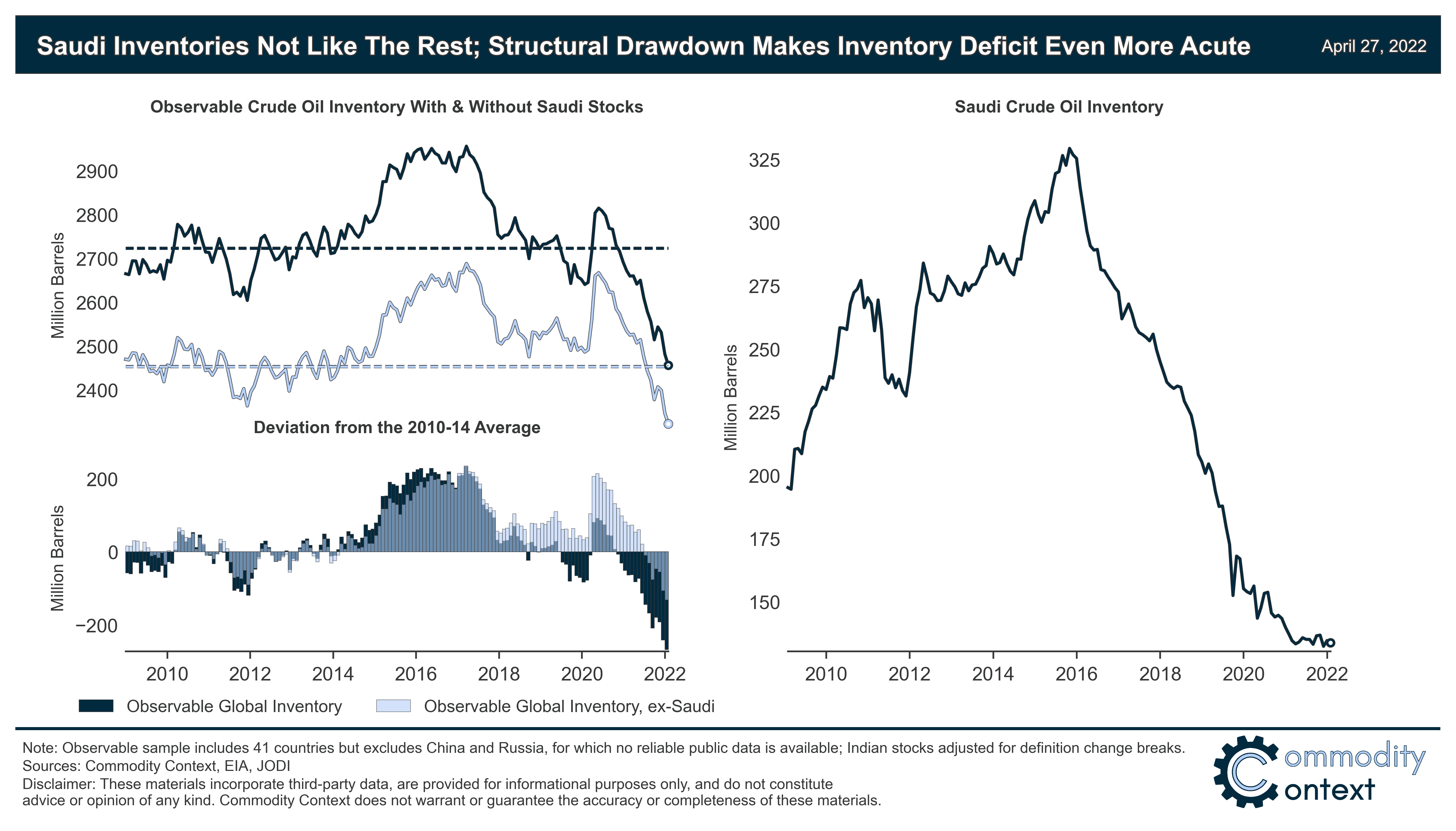

Saudi Arabia Marie Kondo’d its Crude Stocks

An even more fascinating caveat to these global oil inventory measures is how to account for Saudi Arabian oil inventories, which, while small relative to the US, remain among the largest worldwide (unsurprisingly for the world’s largest crude exporter). Saudi inventories have very much cut their own path that is distinct from the pattern of virtually all other inventory holders: Saudi stocks built up through 2016 to nearly 330 million barrels, before nearly straight-line collapsing by more than two-thirds of that today. Strikingly, these reserves didn’t even rise at the depths of the Spring 2020 COVID demand collapse when inventories elsewhere in the world ballooned to record highs—which suggests something is going on here.

There are an assortment of potential explanations with varying merit, but it seems reasonable to assume that the shift from building to winding down crude stocks was due to some combination of: less operational need due to a shift away from US exports toward Asia; the rise of MBS in late-2015; the desire to reduce vulnerabilities to counterattacks related to the war in Yemen; and reduced dependence on direct crude burn for power generation. It’s also important to note that this drawdown doesn’t appear related to any “subsidizing” of the Kingdom’s production level and in any event remains tiny at fewer than 100 thousand barrels per day or less than 1% of the Kingdom’s 10 million barrel a day production rate.

Ultimately, this Saudi destocking does represent a significant 200-million-barrel loss from global crude inventory, but this drawdown should be recognized as largely separate from the forces that have depleted visible stocks elsewhere in the world.

Conclusions

Observable global oil inventories fell at their fastest pace on record and are today around their lowest level in more than a decade. While it’s too soon to determine that our current position represents a truly critically low level of inventory, it’s undeniable that we’re closer to that threshold than we’ve been in a very long time. This wafer-thin safety cushion makes the extreme volatility and wide forecast error bands looking out over the coming year all the more concerning, and a continuation of the past year’s inventory drawdown pace would bring us into truly uncharted territory.

Clicking the LIKE button is one of the best ways to support my research.

Great report Rory. Exceptionally informative.

Concise and original. Awesome work man