Baby, it ain’t cold outside—yet

North American natural gas rally gotta go away, at least for now

North American natural gas prices have fallen from a 13-year high of more than $6.30/MMBtu to just less than $4/MMBtu, largely reflecting a combination of marginally warmer than usual winter temperatures as well as the reduced tail risk probability of an especially cold overall winter (e.g., 2013-14) in forward forecasts.

The outlook for North American natural gas remains firm on the back of structural tailwinds; but winter weather drives winter prices—and temperatures have been pretty mild. Anticipate that pricing will continue to evolve in line with realized weather and forward-looking global weather models.

There is still plenty of time for an especially cold snap to propel natural gas prices higher once again, but the chance of a truly freezing, inventory-depleting winter is lessening as we progress through what has thus far been an uneventful heating season

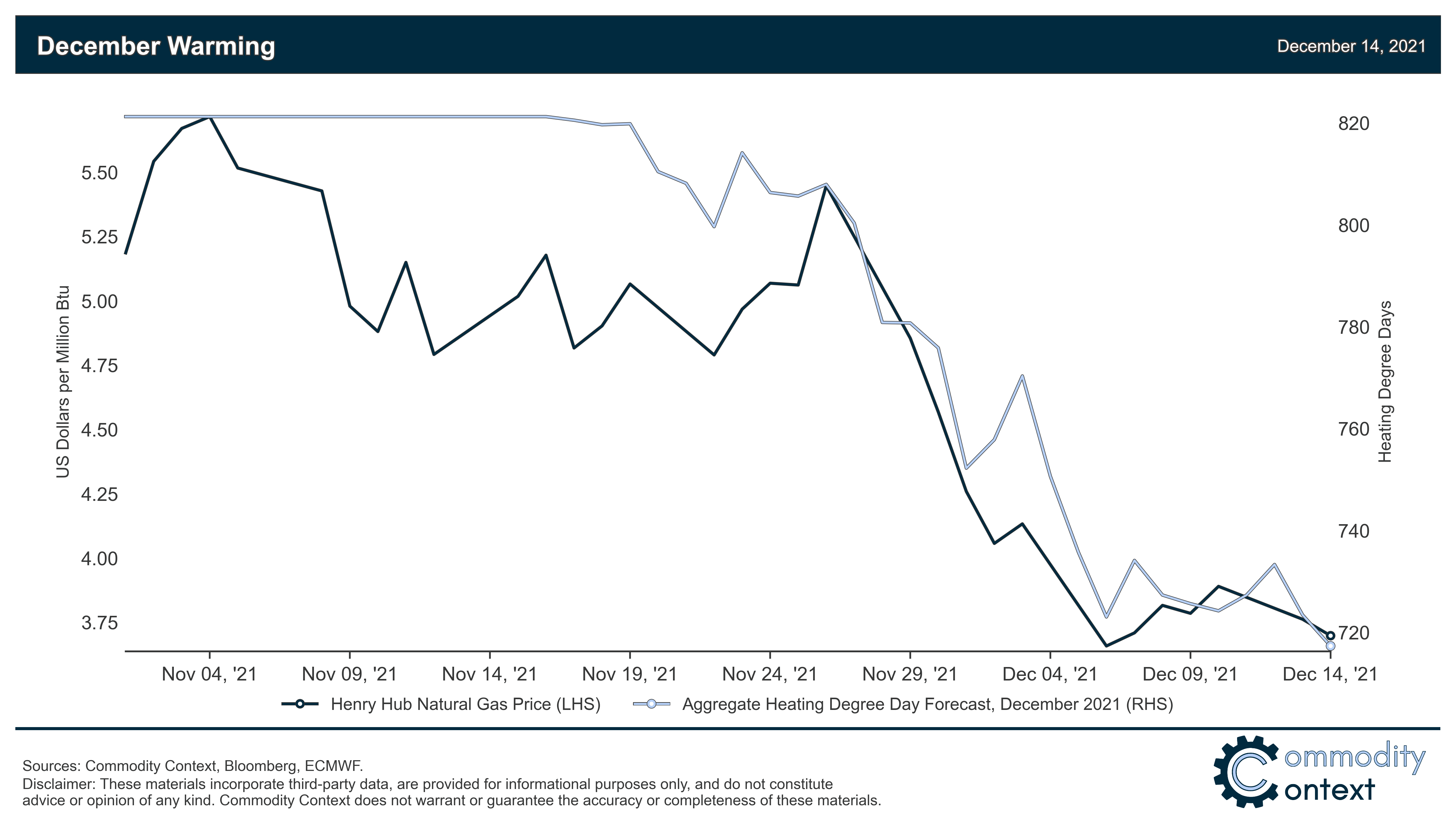

The North American natural gas rally that brought Henry Hub prices to a 13-year high of more than $6.30 per Million Btu (MMBtu) has fizzled over the last month and a half, with prices down more than 40%. Now, $4/MMBtu is still pretty darn lofty for natural gas by the standard of the past half-decade—hell, high-$3s is solid; yet we’ve come down a far way off the $6+ levels of a month ago and you can lay the blame squarely on the [relatively] mild weather.

Note: analysts (and these charts) often use “heating degree days” (HDDs) when looking at the relationship between temperature and natural gas demand, which is a measure of the distance between a given ambient temperature and the temperature to which you’d heat a building for human comfort. To maintain 65° Fahrenheit (18° Celsius) indoors when the average temperature outside is 45°F would equal 20 HDDs, while 60°F outdoor temperatures would mean 5 HDDs. The higher the HDDs, the colder the weather.

Warmer winter brings natural gas prices lower

Prices have since adjusted considerably as we more-or-less track a touch milder than the average winter temperatures, moving us far from that tail-risk inventory-depleting chill that the market was pricing in a month or two ago.

While many claimed that the run-up to $6+/MMBtu was just a speculative mania driven by sky-high prices in Europe and Asia, there was an underlying low-probability but high-impact risk that the already-lower effective inventory position could be further depressed to critical levels by an especially cold winter. Even a 10% chance of a sufficiently large weather-driven price move could have justified these material precautionary price gains.

Heating demand isn’t most important, but it’s often most urgent and uncertain

Residential and commercial heating demand is no longer the largest end-use of natural gas in the US (28% in 2020 vs 38% for power generation), but there is a lot of seasonal variation in heating consumption—so big swings in weather can drive big swings in prices, nonetheless.

As a share of total gas demand, heating demand ranges from as little as 10% in August to 45% in January. In a normal year, half of total heating demand falls, unsurprisingly, between December and February. But winter temperatures also shift materially from year to year, with heating’s demand share peaking at 50% in the brutal winter of 2013-14 vs the only 40% in the winter of 2019-20.

Given the innate difficulties in predicting weather, the market for temperature-dependent commodities –like natural gas—typically prices in something close to average seasonal temperatures when forecasting winter balances and inventory cover. Therefore, pricing evolves in line with both realized weather, which drives actual consumption, and the shifting outlook of global weather models, which estimates future consumption as we progress through heating season.

Don’t write-off winter just yet

North American natural gas will continue to benefit from structural tailwinds, including market share gains in electricity generation (from 28% in 2014 to 41% in 2020), the build-out of a global-scale US LNG export industry (from nothing in 2015 to more than 10% of total supply today), and a lackluster COVID-era supply response despite lofty prices. But still, winter temperatures will always drive winter prices.

Winter is just beginning and, even amidst these increasingly mild forecasts, the season always has the option to throw another polar vortex your way. This can have big market impacts, since the risk of an extreme weather event isn’t typically priced in prior to it fully materializing. For example, you can see above how the increasingly cold outlook in February 2021 boosted the price of natural gas alongside the development of the brutally cold Winter Storm Uri.

The beginning of the 2021-22 heating season has been milder than tail-risk watchers feared, which has vastly reduced the precautionary upside price pressure experienced over the past few months. There is still plenty of time for an especially cold snap to propel natural gas prices higher once again, but the chance of a truly freezing, inventory-depleting winter seems far lower today. While prices are still pretty darn strong overall, the milder outlook allowed natural gas markets to shed some of that insurance buffer, which they’ve gone ahead and done in a hurry.

Thanks. This was great general intel on the Nat Gas market which has proved accurate. Ill give it a share.